SMM reported on June 30:

As 2025 reaches its halfway point, reviewing the first half of the year, the tight supply situation in the domestic zinc concentrate market has eased somewhat. As of June 27, domestic zinc concentrate TCs have risen from 1,950 yuan/mt (metal content) at the beginning of the year to 3,800 yuan/mt (metal content), while imported zinc ore TCs have increased from -$20/dmt at the beginning of the year to $65.25/dmt, with both domestic and imported zinc concentrate TCs climbing steadily.

Limited new capacity additions for domestic zinc ore; production basically flat YoY in H1

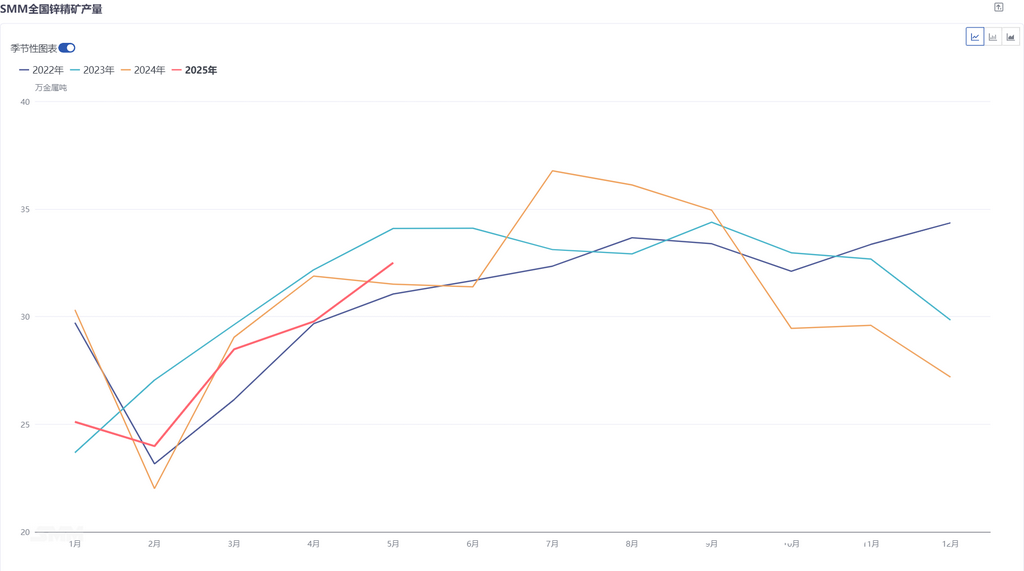

According to SMM data, domestic zinc concentrate production from January to May 2025 totaled 788,300 mt, a 0.06% decrease YoY. In terms of new capacity, some zinc mines that commenced production last year continued to ramp up production this year, and the Huoshaoyun mine also began producing in May this year, bringing a certain increase compared to last year. For existing capacity, with the return from the Chinese New Year, lead-zinc mines in some northern regions of China gradually resumed production, with the overall resumption progress basically in line with market expectations, supporting a continuous increase in domestic zinc ore production in H1. However, due to disruptions in raw ore grade in some regions of China, production at some miners declined, coupled with reduced output from some mines nearing the end of their lifespan, resulting in a basically flat YoY zinc ore production in H1 amidst increases and decreases.

Looking ahead to H2, the continuous ramp-up of production at the Huoshaoyun mine will bring a significant increase in domestic zinc ore production. Additionally, June is basically at the tail end of domestic zinc ore production resumptions. Considering the seasonal pattern of domestic zinc ore operations, production at these resumed mines will continue to recover in Q3, while Q4 is the peak period for domestic zinc ore maintenance, coupled with the temporary shutdown of some northern mines at year-end. It is expected that zinc ore production will increase first and then decrease in H2, possibly reaching the annual production peak in July/August.

Newly commissioned and expanded zinc mines gradually ramp up production; overseas zinc ore production is expected to increase by approximately 400,000 mt YoY

Looking at Q1. According to SMM's production statistics of 20 major overseas miners, from the disclosed financial data, the total zinc concentrate production of these 20 miners in Q1 2025 was 1.297 million mt, an increase of 78,800 mt (6.47%) compared to 1.2182 million mt in the same period last year. The main increases came from the resumption of production at the Tara mine, the ramp-up of production at the Buenavista zinc mine and the Kipushi zinc mine, and the production recovery at the Antamina zinc mine.

Entering Q2. There were not many disruptions to overseas zinc mines in Q2. Although the Antamina zinc mine halted production due to an accident in April, production recovered quickly, and the impact was limited. Although the zinc mine under Canadian miner Hudbay Minerals suspended operations due to wildfires, due to the good operational performance of Snow Lake since the beginning of the year, it is expected that the company will still maintain its full-year operational guidance for 2025 unchanged. Moreover, Australian miner Polymetals Resources Ltd announced that its Endeavor silver-zinc mine in the Cobar region of New South Wales has achieved commercial production, expected to bring a certain increase. SMM forecasts that zinc mine production will continue to grow significantly YoY in Q2, supported by the ongoing recovery of existing mine output and the ramp-up of newly commissioned mines.

Significant Overseas Zinc Mine Growth Drives Recovery in China's Zinc Ore Imports

According to customs data, China's zinc concentrate imports totaled 2.204 million mt in January-May 2025, up 52.46% YoY. On one hand, the substantial increase in overseas zinc mine production this year, particularly from Kipushi, OZ, and Antamina mines, has flowed into the domestic market. Meanwhile, domestic smelter production gradually recovered in H1, and the MoM rise in raw material demand further encouraged smelters to purchase imported zinc ore to replenish inventories.

Looking ahead to H2, although domestic smelters currently show limited enthusiasm for importing zinc ore, their production is expected to continue climbing. Additionally, long-term contracts for imported zinc ore previously secured by smelters will gradually arrive. Thus, China's zinc ore imports are projected to remain at high levels in H2.

In summary, with the recovery of domestic zinc mine production and the substantial inflow of imported zinc ore, supply in the domestic zinc ore market remains ample, driving zinc concentrate TCs higher in H1. For H2, as new capacities from Yunnan Copper and Wanyang gradually come online, smelter demand for zinc ore is expected to rise significantly. If zinc ore imports fail to sustain current levels, the upside potential for TCs may be limited, with even some downside risks.

》View SMM Metal Industry Chain Database